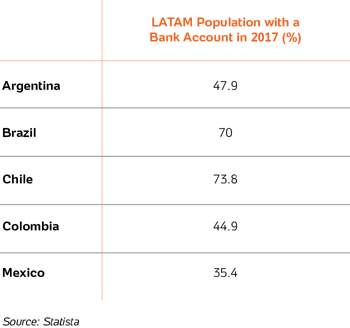

In Latin America, the opening of a bank account can be such an overwhelming process that becomes deterrent and even inaccessible to most people. In fact, it is estimated that more than half of the population does not have a bank account. To open an account it’s necessary to fill in financial paperwork, and to comply with a list of requirements which includes proof of employment, citizenship and, in some banks, to be within the top 20% income bracket. And in some countries, i.e. Brazil, the distance is another barrier.

Based on the inadequacy of traditional banks to decrease the large-scale financial exclusion across the region, there are rising new players in the LATAM banking sector – the digital banks and the neobanks.

What Is Digital Banking and Why Is This Trend Evolving in LATAM

Digital banking provides banking services and solutions through an online platform or a mobile phone app, such as:

- simple transaction services;

- digital payments;

- credit services and alternative funding (such as crowd financing for small businesses and creative/innovative projects);

- personal finance, such as bill pay services and direct deposit of salary.

Unlike traditional banks, digital banks don’t have an in-branch service and customers can do their banking any time, during the day or the night, and any place if there is an adequate internet access. Digital banking has been evolving and is nowadays presenting a model aligned with the increasing of mobile internet access – the neobanks.

Looking at the big picture, it’s clear that neobanks are well-suited to serve Latin America’s young and connected middle-class, whereas that:

- Around 70% of the population is unbanked;

- Latin America had 690 million mobile subscriptions in 2018;

- The mobile phone internet penetration rate was 68.6% in 2018, with 291.4 million users.

As an alternative to traditional banks, neobanks offer convenient and app-driven solutions focused on the customers, while at same time allow them to save on costs (low or free fees). And at a certain scale, neobanks contribute to the financial inclusion with the help of the increasing smartphone penetration, which can drive the usage and development of new digital payment technologies.

Why Digital Banks Leverage E-Commerce in LATAM

Not only customers benefit from digital banking, but it also leverages the e-commerce growth. Take into consideration the above-mentioned facts, add the 71% smartphone penetration rate estimated for 2020, and the 155.5 million of digital consumers expected in 2019, and the result is an immediate understanding that digital banks can potentially enhance e-commerce: they allow consumers to overcome the barriers of having a bank account and to shop online using traditional payment methods, such as credit cards.

On top of that, e-commerce and digital banks work hand in hand empowering consumers and allowing companies to embrace asset-light business models.

Who Is Leading the Trend in Latin America?

Supported by the increasingly relevance that digital banks are having in Latin America, and by the fact that neobanks usually are not associated with any traditional bank, companies throughout the region are emerging as the main characters of this revolution in the banking sector.

Leading the way by the total number of fintech start-ups in LATAM in 2018 are the emerging markets Brazil (380), Mexico (273), Colombia (148), Argentina (116), and Chile (84). Among them are digital banks that are becoming references in their own countries, and in the LATAM region, such as PagBank in Brazil, Albo in Mexico, OmniBnk in Chile, and Ualá in Argentina.

Digital banks are a worldwide fintech trend that is breaking its way through Latin American countries by presenting itself as a solution to a group of adversities – such as bureaucracy, the higher costs of traditional banks and finance exclusion. Digital banks in LATAM have also adapted their services to the local environment – a procedure that is recommended for every international company targeting a fragmented market such as the LATAM region.

Get in touch with us and learn more about how your company can explore the full potential of the region: